In October, U.S. retail sales again outstripped economists’ expectations, posting a 0.4% increase from the previous month, generating optimism about consumer spending resilience as the holiday season approaches. The year-on-year growth also saw a healthy uptick of 2.8%, indicating that, despite economic pressures, consumers are continuing to spend. Although this growth represents a slight deceleration from September’s revised 0.8% increase, it surpasses the forecasted 0.3% rise, signaling sustained consumer confidence.

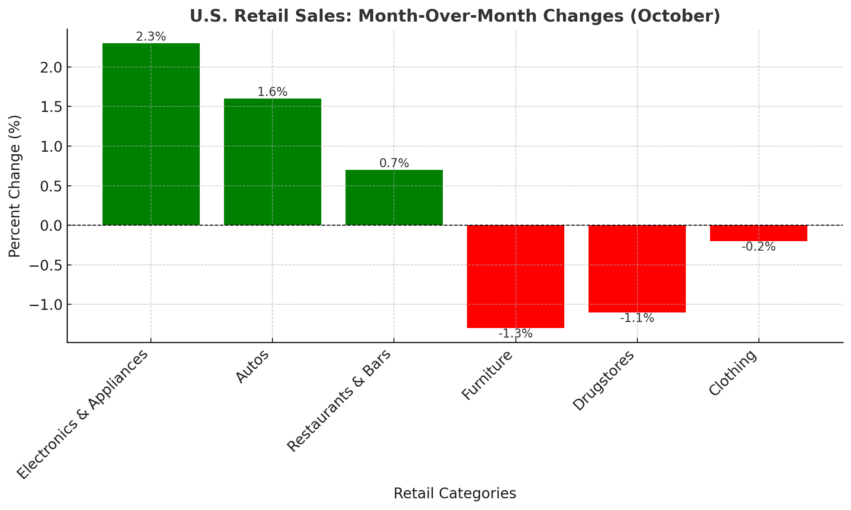

Significant contributors to this uptrend were electronics and appliance stores, which experienced a 2.3% rise in sales. Auto sales also made a substantial impact, advancing by 1.6%. These sectors likely benefited from recent product launches and promotional deals, which tend to draw higher consumer spending. Another notable increase was seen in restaurants and bars, where sales rose by 0.7% month-over-month. This suggests that, in spite of rising dining costs, consumers are still willing to spend on eating out, which often stands as a marker of discretionary spending confidence.

However, not all retail categories enjoyed growth; some faced declines. Furniture stores noted a 1.3% decrease in sales, while drugstores and clothing outlets fell by 1.1% and 0.2%, respectively. These dips could partially be attributed to the disruptive impact of last month’s hurricanes, which not only affected consumer access and shopping behavior but also may have shifted spending priorities temporarily towards recovery and essential goods.

These mixed signals in the retail sector reflect a complex consumer landscape, where economic headwinds like inflation and interest rates contest with a robust job market and steady wage growth. The overall increase in consumer spending, despite being uneven across different retail categories, supports a cautiously optimistic outlook for retail sales heading into the crucial holiday period. As the slowest annual growth pace in three years looms, retailers might still see “decent” performances, assuming that consumer spending power remains stable.

Retailers are likely preparing for the end-of-year rush by strategizing on inventory, promotions, and customer engagement to capitalize on holiday shopping behaviors, especially during Black Friday and Cyber Monday. The real test will be whether this spending strength sustains through the economically and socially significant final quarter, which often sets the tone for the retail industry’s upcoming year.